First-time buyers still don’t know enough about shared homeownership schemes

I agree generally with the article below but what we do not do is look at the reasons why people don’t know about the schemes on offer. I believe they are generally too complex and are designed not to help the First Time Buyer but to help the developers and mortgage industry.

Until Governments look at home ownership from the resident’s perspective and not the vested interests, who want the status quo to continue, we will not move forward and help the 100’s of thousands who need something that the market is not providing currently.

I would argue that Joint Equity does just that – we look at the home ownership in a different way for all parties.

The following article is in Financial Reporter by

AMY LODDINGTON | ONLINE EDITOR, BARCADIA MEDIA LIMITED 24TH MAY 2024

According to the latest research commissioned by Barratt Developments PLC, one in five (20%) first-time buyers (FTBs) aren’t aware of affordable homeownership schemes but, since the general election announcement, Google searches for ‘first-time buyer schemes’ and ‘first-time buyer ISA’ have increased by 5,000% and 70% respectively.

“It’s clear that the housing crisis will be front and center in this election, and we forward to seeing positive policies from all parties aimed at increasing housebuilding, supporting people onto the property ladder,” said David Thomas, Chief Executive of Barratt Developments PLC.

However, the home construction company is concerned that despite this focus, too many first-time buyers (FTBs) are unaware of affordable homeownership schemes due to limited awareness and promotion by the Government. Notably, within an hour of Rishi Sunak’s general election announcement, Google searches for ‘first-time buyer schemes’ and ‘first-time buyer ISA’ have increased by 5,000% and 70%.

What opportunities might be missed due to limited awareness of these schemes?

88% of FTBs expressed unfamiliarity with the mortgage guarantee scheme with only 2,900 monthly searches in the last twelve months, followed by guarantor mortgages (87%), the first home scheme (63%), shared ownership (58%), and lifetime ISA (51%).

“Affordable homeownership schemes are great for helping FTBs get onto the property ladder, and having a variety of schemes available means that they can choose the best fit for them, depending on their circumstances,” said Steve Mariner, Sales & Marketing Director at Barratt Homes.

From an article in Financial Reporter by

AMY LODDINGTON | ONLINE EDITOR, BARCADIA MEDIA LIMITED 24TH MAY 2024

Buying a house: The deposit, the mortgage, and why I couldn’t do it – an article on the BBC web site

Failure of the 95% mortgage market is one of the many reasons why Joint Equity is so popular and allows many more people to live in their own home and benefit from increase in the value of the property.

Many people ask Brad Bamfield, our CEO, why would a Resident Partner use Joint Equity when there are 95% mortgages available?

His answer is “there are 95% mortgages available but for many they are unattainable due to the salary multiple restrictions mortgage lenders apply” this article from the BBC illustrates his point well.

This is an article by

Why can’t I buy a home with a 95% mortgage?

You’ve probably seen at least one – those articles saying you can buy a house aged 21 with a bit of determination and by cutting back on spending.

The people featured usually do have an impressive commitment to the cause of property ownership, saying no to nights out and holidays in favour of basic, home-cooked meals, weekly budgeting and walking everywhere.

But often hidden further down in the piece is a mention of the kind of leg-up that many of us aren’t lucky enough to get: an inheritance from a grandparent or a well-paid role in the family business. Sometimes the person simply lives outside the UK’s most expensive areas.

Such articles can be met with laughter and anger on social media, as people point out that home-buying at a young age really isn’t as simple as having instant noodles for every meal.

Let’s look at some numbers.

The average earnings of 18-21 year olds is around £18,000 a year before tax, according to a government report from last year. If you’re between 22 and 29 years old, the average wage is almost £26,000.

The average house price in the UK was £232,944 in October (and of course houses and flats are available for much less than this, depending on the area). Data shows a rise in the age of first-time buyers to around 30, and older in more expensive areas.

The typical rule for getting a mortgage is that banks will lend you up to 4.5 times your salary. Let’s take the average house price, and assume you have a 10% deposit of 23,000.

You’d need to earn almost £47,000 a year to take out a mortgage for the remaining cost – almost double the average wage for 22-29 year olds.

London, unsurprisingly, is consistently the most expensive place to buy in England and Wales. People there who want to own property can expect to spend up to 13 times their earnings on a home, while for people in North East England, it’s around 5.5 times.

Some areas in the North West are even cheaper – in Blackpool, for example, you could pick up a flat for just over £66,000 or a terraced house for £89,000. But wages there are some of the lowest in the UK, at around £19,700.

‘Want to buy a house? Choose your parents well!’

Buying agent Henry Pryor, a former estate agent who now helps people buy luxury properties, says the market is tough – but your mum and dad’s generation didn’t necessarily have it easier.

“If you want to become a homeowner, you’ve got to choose your parents well,” he jokes. “We have this view that it’s much harder to buy a house now, but I say that’s not quite right. Forty years ago, you couldn’t get a mortgage without a 25% deposit, and interest rates were 15%. Now they’re around 2%.”

He does concede, though, that “it is very hard now – it can be almost impossible for people who don’t have help.”

He does concede, though, that “it is very hard now – it can be almost impossible for people who don’t have help.”

[Brad Bamfield, Joint Equity CEO, says ” Thea illustrates the salary multiple problem well and its true that having parents who can help financially may make the difference but what happens if you do not have a Mum or Dad who can help? This is where Joint Equity becomes a good alternative where we become your Partner and provide that missing support]

Comment from Joint Equity – apart from the salary multiple problem above there are other costs and pitfalls involved some of which Thea reports below. Joint Equity is the buyers’ partner and we have extensive knowledge of and lead the buying process (we buy homes all the time and you will buy 2 or 3 times in your life) – just another headache we remove and reason we are so popular.

‘The stress put me off buying’

Emma, 25, from Nottingham, thought she’d struck gold when she came across a block in Nottingham city centre, where flats were being sold for £100,000 and only a 5% deposit (£5,000) was needed.

“I moved to Oxford after university with a previous boyfriend,” Emma explains. “Even though the relationship didn’t work, the job did, and I stayed there for over two years. Renting in Oxford is so expensive, I couldn’t think about saving. The flat I shared with my ex cost us around £700 a month each. I’ve heard people say living in Oxford is like paying London prices, but not getting a London salary, and I learned that the hard way!”

CONTRIBUTOR IMAGE The Nottingham flat Emma was going to buy

Emma went on to share a flat with a friend, which cost around the same price as before, but when the tenancy ran out she decided to return to Nottingham, where housing was cheaper. She found a job in PR where she earns “under £30,000”, she says – so her earnings are average for her age.

“Rents for a one-bed flat in Nottingham were between £600-800 per month, but a mortgage would be cheaper at about £350,” Emma says. “I was able to save when I moved in with my mum, as I was only paying her about £300, and she did help me with a couple of grand.”

Emma realises she is lucky to live in a location where property is a bit cheaper, and to have a parent who can afford to help her out. For people earning a mid-range salary of around £24,000 in Nottingham, a city centre flat like the one Emma wanted is affordable.

But the bank wouldn’t give her a mortgage because “too many other flats in the building were rented,” she explains. “So many had been bought by private landlords and rented out. So if I wasn’t able to keep up with my payments it would probably make it harder for the mortgage company to then resell it and get the money back.”

“Some mortgage lenders get jumpy if there are lots of renters or Airbnbs in the building,” explains Henry. “They can also refuse a mortgage on buildings made of certain concrete, and sometimes people don’t find this out until too late. There are lots of reasons a mortgage might be refused.”

Emma then found another, similar flat in the same price range, in a smaller block. Her offer was accepted by the seller, and her solicitors began the process of the sale.

“The extra costs were a surprise,” Emma adds. “I was quoted £2,000 for a solicitor, which is around average, but I paid £125 up front, and didn’t have to pay the rest until I’d actually bought the flat. Then there was the mortgage broker – that was £350, but I only paid half up front. The searches and surveys were probably another £300.”

“Remember you’ll have legal bills and you’ll need money for them on top of the deposit,” says Henry. “If you want an extra survey, that might be an extra £1,000. Homebuyer’s insurance – to get money back if something goes wrong – could be about £50. If you’re not prepared, it’s like saying ‘I want to buy a car, but I didn’t know you have to insure it!'”

Six months later, the solicitors still hadn’t progressed, and Emma’s mortgage offer expired. If she wanted to try another bank, she’d have to pay more costs – something she didn’t want to do, because she’d already eaten into her savings.

“The stress of it has put me off buying for a while,” Emma says. “It’s meant to be this exciting thing you do – I was 24 and single and it was a really good feeling. But the fact it took so long and all fell through, I don’t know if I want to go through this again at the moment. When I do try again I might look outside the city centre.”

Emma is still living with her mum, but plans to rent a flat with her boyfriend in the near future. She knows she’s one of the lucky ones, and that buying a property is still within her reach once she saves up the money she lost – something she can do on her salary. But for some, buying looks impossible.

Joint Equity is always looking for new ways to help people move into their own home. Register as a Resident Partner (click here) and be first to know how we can help you achieve your own home with all the security it provides

Buying your home is stressful but even we were surprised by this survey.

We all know buying your home is stressful and it seems everyone concerned with it adds their own problems. Estate agents, sellers, lawyers, mortgage brokers, mortgage lenders, valuers but they can really cause problems for a traditional buyer.

The good news is that if you are a prospective Joint Equity Resident Partner we, and our team of experts, are here to help and we have done in loads of times so we roll over hassles, we lower hurdles and we smooth the path into your home.

So what did the survey find?

One in four (25%) borrowers say they found the traditional mortgage application process to be stressful, while 5% felt compelled to complain to their lender or broker about the service they received, according to research from Trussle, the online mortgage broker.

One in four (25%) borrowers say they found the traditional mortgage application process to be stressful, while 5% felt compelled to complain to their lender or broker about the service they received, according to research from Trussle, the online mortgage broker.

Close to one in ten (8%), or about 27,000 homeowners admit they were reduced to tears while attempting to secure their first mortgage.

While 23% were forced to take time off work to make arrangements for their first mortgage. Applied to last year’s 338,000 first-time buyers, this equates to 77,740 people taking a day off in 2016.

The negative experience so often associated with securing a mortgage is also leading to inertia among current borrowers. One in ten (9%) respondents, the equivalent of a million people, say they’ve been discouraged from switching mortgage by their experience of being a first-time buyer, while for 13%, it’s actually discouraged them from moving home.

Ishaan Malhi, CEO and founder of Trussle, commented: “Buying a home is one of the biggest milestones in someone’s life and should be remembered with fondness, but for so many, it’s an ordeal they’d rather forget. A lot of it comes down to the stress and inconvenience of the mortgage application process. It’s therefore understandable that so many people are reluctant to think about their mortgage when the time comes to switch, but the sad result is that homeowners are collectively losing billions of pounds a year.

“The good news is that things are improving, if in pockets. We’re already seeing dramatic progress in the mortgage customer experience, with the use of technology speeding up and simplifying the whole process. This in turn should help to address some of the causes of the inertia costing homeowners so much money.”

Joint Equity can help

This survey is supported by our own informal survey when we asked what you did not like about the buying process click here for more.

This survey is supported by our own informal survey when we asked what you did not like about the buying process click here for more.

While Joint Equity cannot remove all the problems, as you still have to work with mortgage lenders, our mortgage brokers, who are experienced with the Joint Equity process, will help you over every hurdle, easy to talk to, know how important this is to you and will smooth the way in to your new home.

Do buyers understand Shared Ownership Homes?

The answer, at least from research that My Home Move have completed, seems to suggest no. However, we find that our prospective Resident Partners understand Joint Equity Shared Home Ownership very well.

- So is the problem with the “public” regulated providers such as housing associations and Councils?

- Does the private sector such as Joint Equity do it better?

- Or is there something else that puts home owners off?

My  Home Move have found that shared ownership transactions across England and Wales have decreased throughout the majority of regions, in fact 7 out of 9 regions – including London, the Home Counties, North East, South East, Wales, West Midlands and Yorkshire – and interestingly currently accounts for less than 1% of housing stock across England and Wales.

Home Move have found that shared ownership transactions across England and Wales have decreased throughout the majority of regions, in fact 7 out of 9 regions – including London, the Home Counties, North East, South East, Wales, West Midlands and Yorkshire – and interestingly currently accounts for less than 1% of housing stock across England and Wales.

Just two regions, the East of England and East Midlands, saw a rise in shared ownership transactions between January and August 2017 compared to the corresponding months in 2016 and even in these regions, shared ownership counts for less than 1% of all completions, at 0.7% and 0.6% respectively.

In a survey of aspiring first-time buyers, only 11% said they were looking to buy a shared ownership home, while nearly 80% were looking to purchase a home outright.

In a survey of aspiring first-time buyers, only 11% said they were looking to buy a shared ownership home, while nearly 80% were looking to purchase a home outright.

However, nearly 30% admitted to not understanding what shared ownership is. However, the English Housing Survey found 1 in 10 people live in Housing Association homes but does not differentiate rented from shared home ownership.

Doug Crawford, CEO of My Home Move, said: “Last February the Government pledged to fix Britain’s broken housing market, and yet one of the schemes designed to encourage home ownership is falling in popularity. Our research highlights just how small transactional volumes for shared ownership are, raising questions as to whether the scheme needs to change its image to attract new home buyers.”

“It’s our belief that home buyers, despite the lack of housing stack, are turned off by phrases like ‘affordable housing’, which is often used to describe ‘shared ownership’. Yes, they want to be able to afford their home, but they want to buy a dream.

The idea of buying a home that has been built to fulfill a quota, or is being sold through a housing association and so has the negative connotations of social housing attached to it, is just too much for some.

Perhaps we need to ‘rebrand’ the image of shared ownership, to bring it in line with initiatives like the Government’s Help to Buy, to make it more attractive to first time-buyers.”

Doug also said “With these findings in mind, we think there is a missed opportunity for those involved in shared ownership schemes, to educate aspiring first-time buyers better. Shared ownership can offer those trapped as ‘generation renters’ a real possibility of getting onto the property ladder, but it’s all a question of selling them the dream and maybe it’s time to find out what would make aspiring first-time buyers change their mind.”

How is Joint Equity and shared home ownership different?

Now we at Joint Equity do not sell a dream, we hate that phrase, we help renters deliver their own dreams; by Partnering with us and achieving together what we cannot accomplish alone. That does not just include a home but it includes improving our life and status.

Doug is right however, when he says shared home ownership has a stigma, who wants to be part of a quota, who wants to be seen as requiring “affordable homes” and relying on financial help?

Another big turn off, you tell us, is the intrusive application forms from housing associations and the way mortgage lenders look at “public” shared ownership and the connection with housing associations.

Joint Equity is “tenure blind”, if you buy a home in Partnership with us, whether it is one of our new builds or its old stock you have found, your neighbours will never know your ownership is any different from theirs. You do not stand out as different.

Joint Equity is “tenure blind”, if you buy a home in Partnership with us, whether it is one of our new builds or its old stock you have found, your neighbours will never know your ownership is any different from theirs. You do not stand out as different.

In fact many of our Resident Partners seem to be proud of the Partnership with us, the support we give, the benefits we give and the security we give.

And we are equally proud of each and every one of our Resident Partners in having dreams and striving to achieve them. When our Partners move on to a home where they do not need our help we celebrate their success, when they buy out our Share we celebrate their success and even when we help an aspiring Resident Partner get their own mortgage without our help – yes you guessed it – we celebrate their success.

Why do we do this and more? Because we believe in Partnership and we are possibly the only shared home ownership provider that does.

So does shared home ownership need a “rebrand”, does it need to be made more attractive, less of a stigma around the name and process – the answer is yes.

Does Joint Equity need a rebrand, to be made more attractive, less of a problem – we think no, our Resident Partners seem to think no, the 2,400 people who are considering buying through Joint Equity seem to think no.

Home ownership impossible for one in four young Brits says Halifax Building Society Report

Home ownership has sailed for one in four young Brits says Halifax Building Society Report

The headlines from the report:-

- There are approximately 19.5M young Brits in the UK.

- 25% (4.8M) of 18-34 year-olds are relying on inheritance to get on the property ladder

- One in 10 (1.9M) young people would leave the UK for a more affordable home

- 25% (4.8M) are certain they’ll never own their own home

- One in five (3.9M) says home ownership is a thing of the past

Almost half (48%) of young Brits think it’s harder than ever to get on the property ladder, with one in 10 prepared to leave the UK in order to buy their own home.

New research from the Halifax uncovered the attitudes of young people who don’t own a property, revealing that a quarter of 18-34-year-olds think the only way they’ll manage is by inheriting the cash.

Eight out of 10 feel that a lack of affordable property is keeping home ownership out of reach, and as a result one in 10 (14%) think they’ll need to rent forever.

However, first-time buyers end up on average £651 a year better off buying than renting.

Despite the number of first-time buyers reaching a 10-year high of 339,0001 in 2016, half of 18-34-year-olds don’t think home ownership is a realistic option for their generation – with two thirds (65% or 12.6M people) saying they don’t earn enough to afford it.

Unsurprisingly, deposits remain too unrealistic and expensive for more than half (52%) of young people as the average age of those buying their first home has crept slowly up to 30.

More than half of young people feel that the average house price for a first home in their area is currently unrealistic for them, causing generation rent to think about relocating to boost their chances of buying.

One in five (22%) 25-34 year-olds would move to a cheaper area and even more of their younger counterparts aged 18 to 24 would be prepared to pack their bags for a bargain home elsewhere in the UK.

One in five (22%) 25-34 year-olds would move to a cheaper area and even more of their younger counterparts aged 18 to 24 would be prepared to pack their bags for a bargain home elsewhere in the UK.

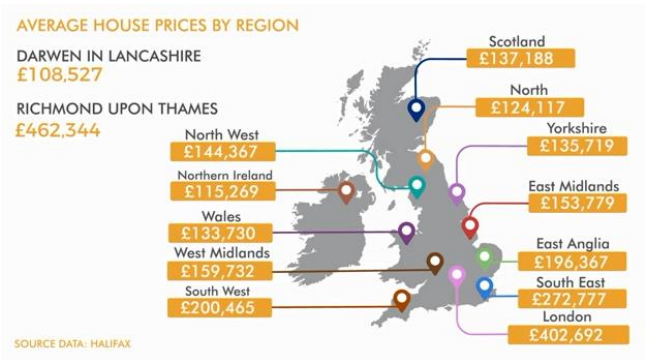

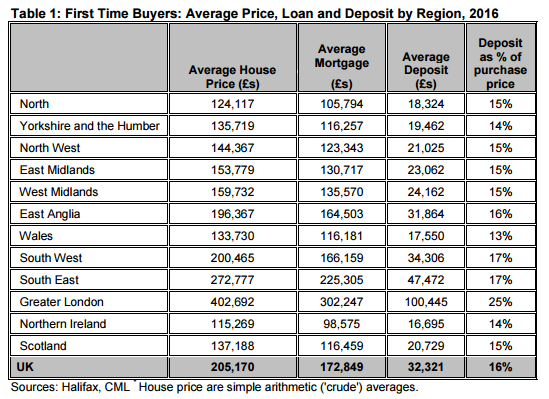

The average deposit put down for an average first-time buyer home is £32,3212 , rocketing to £100,445 in London. Northern Ireland has the lowest at £16,695 – less than half of the average deposit needed in the South East (£47,472).

Martin Ellis, Halifax housing economist, said: “Even with the highest number of first-time buyers in the last decade in 2016, many young people still feel they are running financial gauntlet – saving for a deposit, finding an affordable property in the right area and managing to fund living in the meantime.

“It’s never too early to do some research to help build a better understanding of how much is affordable, the borrowing options available and calculating what’s achievable to help make owning a property more of a reality.”

Although aspiring homeowners could begin gravitating towards the UK’s more affordable areas to get on to the property ladder, more than one in five (22%) feel that home ownership is a thing of the past.

Even if they have managed to raise a deposit, a third (33%) feel mortgage criteria is too difficult for them to meet.

Brad Bamfield, founder and CEO of Joint Equity, said

“this supports the feeling of many in the property industry that young people have been “put off” owning their own home. Our evidence from the emails we receive is quite the opposite where the desire to own is stronger than ever its just that over regulation and the movement to the so called risk adverse lending in the industry has led to fewer opportunities for buyers.”

Joint Equity has been supporting the First Time Buyers, Divorced and Separated and Retired Renting to make the first steps in home ownership since 2007.”

Brad continued “today we need a range of products to serve the home owning aspirations of people today and unfortunately our finance industry is so frightened of new approaches and products that they will find every excuse not to do something and it’s people excluded from the market that suffer and are driven into the clutches of unscrupulous landlords and their letting agents.”

How does Government schemes to help home buyers compare to Joint Equity

If you’re one of millions of people that don’t have access to family financial support, there are a range of Government Schemes to help you take your first step on the ladder and we outline the key points below.

Then we look at the Joint Equity Shared Home Ownership scheme for comparison. Well we would wouldn’t we!

Help to Buy

First-time buyers can open a Help to Buy ISA, which gives a 25% government bonus on amounts saved between £1,600 and £12,000 – although the bonus is capped at £3,000.

First-time buyers can open a Help to Buy ISA, which gives a 25% government bonus on amounts saved between £1,600 and £12,000 – although the bonus is capped at £3,000.

It can be used for any property costing under £250,000 (£450,000 in London) and any mortgage.

You can save up to £1,000 in your first month, then up to £200 a month after that. You can choose to pay in less if you want, and it’ll still work.

Help to buy ISAs are only available to individuals. If you’re buying together, you can separately claim the government bonuses on your savings – and then combine the two to form a joint deposit.

Things to note:

- The deadline to open an account is December 2019. In April 2017, help to buy will relaunch to become the government’s lifetime ISA . But you will be able to shift your money across tax-free.

- It’s a monthly saving scheme but if you miss a contribution one month, you can’t make up for it in the following month (the cap is £200).

- If you’re buying together, but one of you is already a home owner. The first time buyer can still open an account.

- You need to get your solicitor to apply for the bonus when you buy a home. Alternatively, you can take the money out at any point, but if you choose this, you won’t qualify for the bonus.

- If you’re saving into a help to buy ISA you can’t save into another cash ISA in the same tax year.

More on Help to Buy ISA http://www.moneysavingexpert.com/savings/help-to-buy-ISA

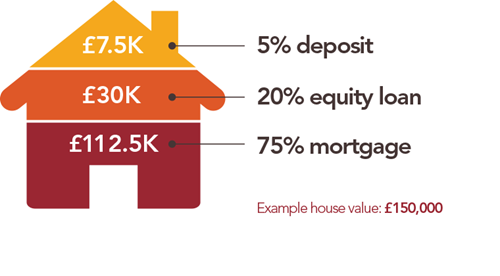

Help to Buy Equity Loan.

The remaining part of help to buy scheme is called the Equity Loan. It requires a minimum 5% deposit of the property value with the government offering an interest-free loan of a further 20%. The remaining 75% is covered by a standard mortgage.

As Zoopla explains, to buy a £200,000 property under the equity loan scheme, you’d need a minimum deposit of £10,000 and to qualify for a £150,000 mortgage. The government then provides an equity loan of £40,000.

How does it work?

How does it work?

- There is no interest to pay for the first 5 years.

- In year 6, interest (known as a ‘loan fee’) kicks in at 1.75%.

- The rate increases every year thereafter at the RPI (retail prices index) measure of inflation plus 1%.

- The idea with the help to buy equity loan is that, because you’re theoretically only borrowing 75% from the mortgage lender, rates will be cheaper than on a 95% mortgage. But don’t assume that’s always the case.

- When you come to sell your home, the government will take back its 20% share of the sale price.

This option is only available on new-build properties worth up to £600,000. The scheme will remain open until 2020.

Lifetime ISA

In his 2016 Budget, Philip Hammond announced a new lifetime ISA which will launch in April 2017. This will replace the current help to buy ISA – you’ll be able to shift your money across tax-free.

- You can only save a maximum of £4,000 a year

- The account offers a tax-free boost of up to £1,000 a year towards either buying your first home or saving towards retirement.

- Savers aged 40 or under can open these accounts, which will become available from April 2017. You can put away up to £4,000 each year. The government will then boost returns by 25p for every £1 saved at the end of each tax year.

- If you’re a first time buyer, you can then opt to use your lifetime ISA cash as a deposit on a property worth up to £450,000.

- If you save the maximum for 5 years you will have £20,000 + £4,000 bonus

Finally the penalty – if you save £1,000 the Government will give you £250 seems a good deal (but remember the maximum you can get is £1,000 bonus a year not to be sniffed at but not its not huge sums) and if you need the cash for any other purpose than buying a home you have to pay a penalty of 25%.

But here is the rub its calculated on 25% of the total which is £1,250 and so the penalty is £312.50 leaving you just £937.50 or £62.50 less than you saved. That is the penalty you pay.

So beware taking your money out for any reason other than buying a home or at retirment is costly

More Lifetime ISA http://www.moneysavingexpert.com/savings/lifetime-ISAs

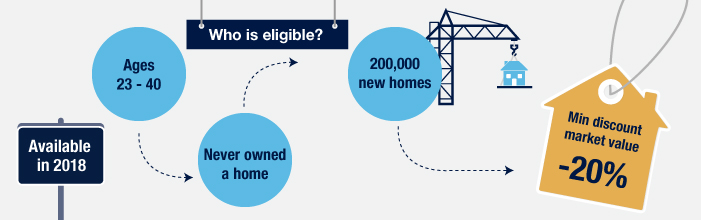

Starter Homes scheme

In March 2015, the government proposed a new Starter Homes Initiative. In January this year, it said work on the new scheme had commenced.

In March 2015, the government proposed a new Starter Homes Initiative. In January this year, it said work on the new scheme had commenced.

This will see the creation of around 200,000 new ‘affordable’ homes, sold at a minimum discount of 20% to first-time home buyers aged between 23 and 40. Construction of these homes started in January 2017 – and the properties could be ready to sell as early as January next year.

There’s a £250,000 price cap on homes available under the scheme, rising to £450,000 if you’re buying in London.

Beware though developers build homes to make money so expect low specifications, small sizes ad corners to be cut.

Shared Ownership.

Shared Ownership schemes allow you to purchase just share of a home (between 25% and 75%) from a local Housing Association and pay rent – up to 3% – on the part you don’t own.

Under a process known as ‘staircasing’ you’ll then be given the chance to buy back chunks as and when you can afford to until you own 100% of the home. These chunks will be priced at the home’s current market value as assessed by the Housing Association. You will also have to pay a valuer’s fee each time.

To qualify for Shared Ownership, your household income must not exceed £80,000 or £90,000 if you’re buying in London.

Housing Associations have strict rules and eligibility can be a problem if you do not have enough “need” as they define it.

The application process is tortuous at best and you can only buy the properties they have on offer in the locations they have built in.

More here http://www.zoopla.co.uk/shared-ownership/

Joint Equity Shared Home Ownership

So how does Joint Equity Shared Home Ownership compare?

As you know the Resident Partner buys 50% of the home and Joint Equity contributes the other 50%.

As you know the Resident Partner buys 50% of the home and Joint Equity contributes the other 50%.

- It’s a simple to understand scheme based on real Partnership between the Resident Partner and the Investment Partner.

- You can use your Help to Buy or Lifetime ISA to buy your Share as long as you have a mortgage as well.

- You cannot staircase above 50% but you can offer to buy out the Investment Partner 50%.

- If you sell your Share the Investment Partner may buy it from you and the gain you make is all yours.

- You pay a Non Resident Partner payment for the 50% you do not own, the same as the Housing Association rent, but with Joint Equity its not a rent and there are no rental conditions attached.

Joint Equity does build homes for sale in the Joint Equity Shared Home Ownership scheme but because we are 50% Partners with the Resident Partner we build real homes for people to live in, to high specifications, with large airy rooms. We build for the future value of our Share not for the sale price today and walk away from the future value like developers and builders.

But Joint Equity will also join with you to buy any second hand home that you like and want to live in. Its not for nothing we say

Any home, any where.

Finally we are your Partners as long as you stay with Joint Equity and we are always here when you need help and advice with anything to do with your home, we will also contribute to improvements that raise the value of your home.

So Joint Equity is simple, easy to live with and a real Partnership and that makes living in your own home with our help rewarding, profitable and secure.

Some of our Partners have been with us over 10 years now and say they never want to leave.

Retired and still renting – a concerning trend

Joint Equity now helps retired people who are trapped in rental properties buy a home of their own. We have always helped first time buyers and divorced and separated but the demand from older would be buyers who have perhaps been refused mortgages or believe they will never have the security of their own home is overwhelming.

In the 2011 census there were 4.2m households living in private rented accommodation. 50% of the head of household were in the 50 to 75 age group – that is over 12m households. 50% of these people declared themselves as economically inactive. The majority said this was because they were retired. That is a staggering 3m households.

In the 2011 census there were 4.2m households living in private rented accommodation. 50% of the head of household were in the 50 to 75 age group – that is over 12m households. 50% of these people declared themselves as economically inactive. The majority said this was because they were retired. That is a staggering 3m households.

In the 50 to 75 age group just over 25% were renting and – using the same proportion of social to private sectors. This suggests that over 350,000 households are retired and living in the private rented sector.

“At later stages in life, where security and peace of mind is even more of a priority, it’s concerning that such a significant percentage of our retired population is having to endure the uncertainty, and many other issues, that come with renting a property, “ says Brad Bamfield CEO of Joint Equity.

“There are so many unappealing aspects of rented living – the prospect of having to regularly move, the upheaval, the concerns about rising rent prices. A priority must be to educate people more about the alternative home ownership options available to them. There are new ways to escape the rental market, take control of your housing finances and own your own home.”

If any of the following questions strike a chord with you, as it does many of our current Resident Partners over a “certain” age, and you answer yes then you need to read on and see how Joint Equity can help you now because if you can afford to rent you can afford to buy with Joint Equity.

- Are you retired and living in rented property?

- Do you dislike the insecurity of rented accommodation?

- Worried about future rent rises?

- Do you have savings that earn you next to nothing?

- Do you think you can never live in your own home with all the security that provides?

Joint Equity can help change things for the better.

You own 50% and we own the other 50% in Partnership. So any growth in the property is shared 50/50 between us and when you sell your Share in the property you get your deposit back as well.

And we do this often for less than the cost of renting.

Remember we are not your landlord we are you Co-owning Partner and its absolutely your home with complete security to stay there as long as you want.

Your investment in your home can be passed on to your heirs together with your share of the increase in value, we are not Equity Release taking great chunks of your value. Nor do we interfere in your life while you live in your home however, we are always available 7 days a week if you need advice or help with the home – we are you Partner after all.

Brad Bamfield CEO of Joint Equity said “the retired renting sector is very important to us as security becomes more important the older you become. We all remember when we were young nothing was frightening and moving every year or so was exciting. “

Brad Bamfield CEO of Joint Equity said “the retired renting sector is very important to us as security becomes more important the older you become. We all remember when we were young nothing was frightening and moving every year or so was exciting. “

“This is not the case when you are over 60 when change and upheaval, usually not through your choice but usually imposed by your landlord, is frightening, difficult and deeply upsetting.”

“Joint Equity offers a real alternative to many people in this sector offering peace of mind, security and a real Partnership for the future years.”

Joint Equity offers an alternative for retired people living in rented accommodation and a viable, secure way of owning your own home. For more information find out about how to become a Resident Partner www.jointequity.co.uk and check out our video page https://www.jointequity.co.uk/videos/ for a real life Resident Partner and her experience.

Sources: Housing Census headlines here