Joint Equity now helps retired people who are trapped in rental properties buy a home of their own. We have always helped first time buyers and divorced and separated but the demand from older would be buyers who have perhaps been refused mortgages or believe they will never have the security of their own home is overwhelming.

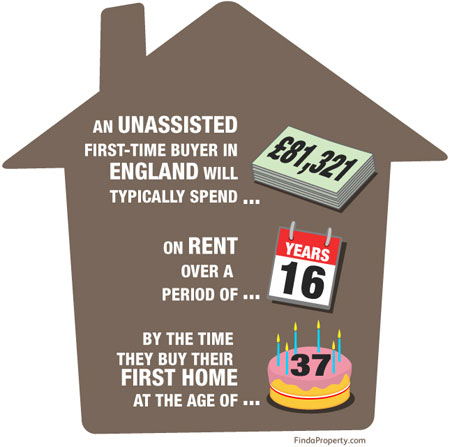

In the 2011 census there were 4.2m households living in private rented accommodation. 50% of the head of household were in the 50 to 75 age group – that is over 12m households. 50% of these people declared themselves as economically inactive. The majority said this was because they were retired. That is a staggering 3m households.

In the 2011 census there were 4.2m households living in private rented accommodation. 50% of the head of household were in the 50 to 75 age group – that is over 12m households. 50% of these people declared themselves as economically inactive. The majority said this was because they were retired. That is a staggering 3m households.

In the 50 to 75 age group just over 25% were renting and – using the same proportion of social to private sectors. This suggests that over 350,000 households are retired and living in the private rented sector.

“At later stages in life, where security and peace of mind is even more of a priority, it’s concerning that such a significant percentage of our retired population is having to endure the uncertainty, and many other issues, that come with renting a property, “ says Brad Bamfield CEO of Joint Equity.

“There are so many unappealing aspects of rented living – the prospect of having to regularly move, the upheaval, the concerns about rising rent prices. A priority must be to educate people more about the alternative home ownership options available to them. There are new ways to escape the rental market, take control of your housing finances and own your own home.”

If any of the following questions strike a chord with you, as it does many of our current Resident Partners over a “certain” age, and you answer yes then you need to read on and see how Joint Equity can help you now because if you can afford to rent you can afford to buy with Joint Equity.

- Are you retired and living in rented property?

- Do you dislike the insecurity of rented accommodation?

- Worried about future rent rises?

- Do you have savings that earn you next to nothing?

- Do you think you can never live in your own home with all the security that provides?

Joint Equity can help change things for the better.

You own 50% and we own the other 50% in Partnership. So any growth in the property is shared 50/50 between us and when you sell your Share in the property you get your deposit back as well.

And we do this often for less than the cost of renting.

Remember we are not your landlord we are you Co-owning Partner and its absolutely your home with complete security to stay there as long as you want.

Your investment in your home can be passed on to your heirs together with your share of the increase in value, we are not Equity Release taking great chunks of your value. Nor do we interfere in your life while you live in your home however, we are always available 7 days a week if you need advice or help with the home – we are you Partner after all.

Brad Bamfield CEO of Joint Equity said “the retired renting sector is very important to us as security becomes more important the older you become. We all remember when we were young nothing was frightening and moving every year or so was exciting. “

Brad Bamfield CEO of Joint Equity said “the retired renting sector is very important to us as security becomes more important the older you become. We all remember when we were young nothing was frightening and moving every year or so was exciting. “

“This is not the case when you are over 60 when change and upheaval, usually not through your choice but usually imposed by your landlord, is frightening, difficult and deeply upsetting.”

“Joint Equity offers a real alternative to many people in this sector offering peace of mind, security and a real Partnership for the future years.”

Joint Equity offers an alternative for retired people living in rented accommodation and a viable, secure way of owning your own home. For more information find out about how to become a Resident Partner www.jointequity.co.uk and check out our video page https://www.jointequity.co.uk/videos/ for a real life Resident Partner and her experience.

Sources: Housing Census headlines here

Good to see the word being spread about the Joint Equity model of shared ownership. Read some of our latest press coverage here:

Good to see the word being spread about the Joint Equity model of shared ownership. Read some of our latest press coverage here: