No way out of renting for four in ten tenants

Home ownership is out of reach for 42% of tenants, who say they cannot afford to save for a deposit at all, and other want-to-be homeowners are unable to save enough.

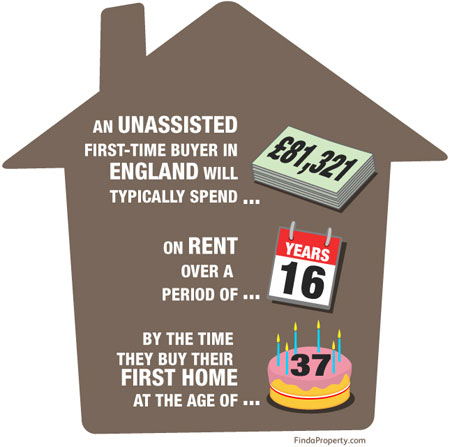

The average amount saved by the 35% of tenants who do save for a deposit is £12,125 – about 7.3% of today’s average house price of around £165,000. That’s significantly less than the 10 to 20% which is typically required (approx. £16,000 to £30,000).

The average amount saved by the 35% of tenants who do save for a deposit is £12,125 – about 7.3% of today’s average house price of around £165,000. That’s significantly less than the 10 to 20% which is typically required (approx. £16,000 to £30,000).

What many people aren’t aware of are the alternative co-ownership options available to them. With Joint Equity, for example, the minimum deposit required is 5% of the home value which for today’s average house is £8,250.

Surprising still is that nearly one-third of tenants are spending more than half their take-home pay on rent, and 35% of those managing to save a deposit are having to dip into it, either regularly or to pay for holidays. Among the under-30s, 60% have already used their home savings pot for other things.

These statistics are all from the property-sharing website SpareRoom, and another interesting and perhaps unexpected statistic shows that the large majority (79%) of those polled described themselves as employed professionals.

Matt Hutchinson, director of SpareRoom.co.uk, said: “A significant proportion of the people we polled expect to live in rented accommodation for at least five years, and many believe it will be much longer than that.

“The facts speak for themselves. Soaring living costs mean it’s a struggle for many households just to keep their heads above water each month, let alone have enough spare cash to put aside towards a deposit. The survey shows that even those who are squirreling away funds have not managed to save anywhere near enough to buy the property they want.”

Brad Bamfield CEO of Joint Equity said, “These stats continue to shock us which is why we’re determined to help educate people about alternative home ownership options. For instance, our Resident Partners can now live in their own home in co-ownership with us on a 50/50 basis. In nearly all cases if you can afford to rent you can afford to buy with Joint Equity.”

Brad Bamfield CEO of Joint Equity said, “These stats continue to shock us which is why we’re determined to help educate people about alternative home ownership options. For instance, our Resident Partners can now live in their own home in co-ownership with us on a 50/50 basis. In nearly all cases if you can afford to rent you can afford to buy with Joint Equity.”

“We aim to help over 25,000 people leave the rented sector for their own home every year and our vision is that no one who does not want to rent should be forced to stay in it longer than really necessary”

For more information visit www.jointequity.co.uk

Our thanks to http://www.spareroom.co.uk/