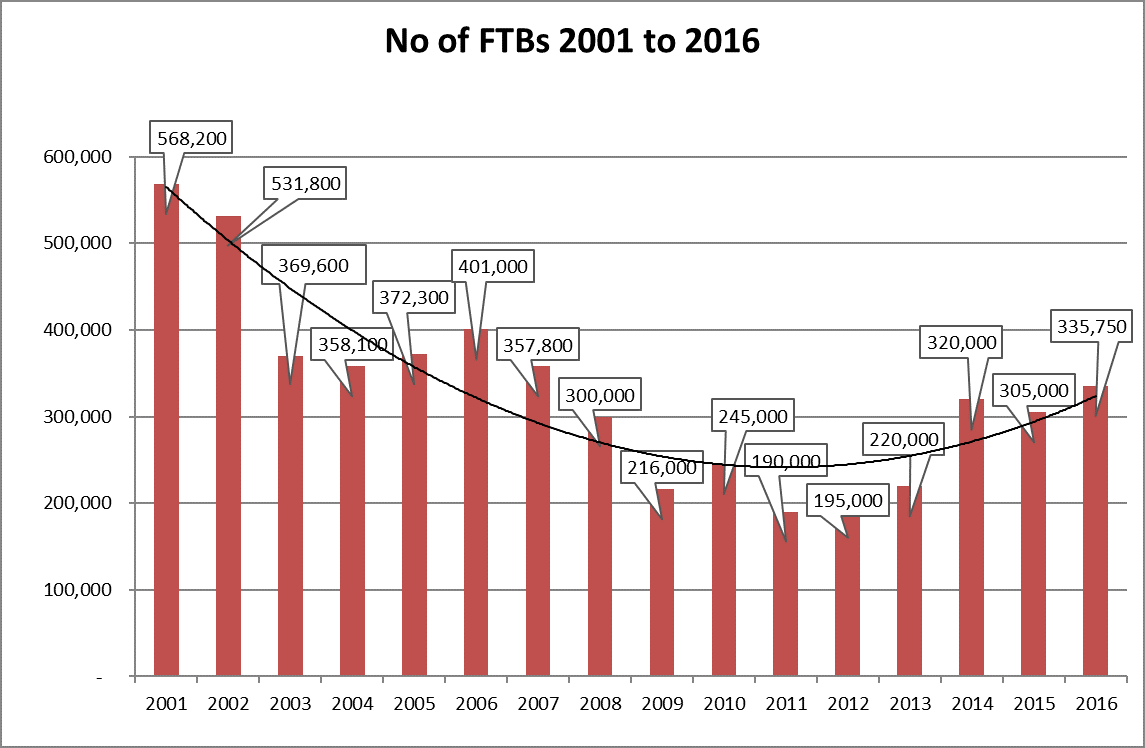

Homeownership is always important to UK people

A new UK-wide study from first direct highlights the meaning of success to people across the UK and reveals what they deem as ‘successful’ and important throughout different stages of their lives.

The research shows that young Brits aren’t deterred by the ever-increasing challenge of getting on the property ladder and are more keen to own their own homes than their parents.

Ambitious and unphased

According to the latest official figures, the typical home in the UK costs £216,674 – up by 6.9% from the previous year. As a result of the rise, the BBC recently reported that first-time buyers would need to find an average deposit of about £33,000 for a mortgage on such a property.

In order to save for a deposit of this amount, first time buyers on the average UK salary of around £27,000 would need to save their full pre-tax wage for at least 14 months.

In order to save for a deposit of this amount, first time buyers on the average UK salary of around £27,000 would need to save their full pre-tax wage for at least 14 months.

Despite the ever increasing challenges, the research suggests that young Brits are more determined than most to achieve the home ownership dream with 71% of 18-34 year olds saying it is important to them to own their own property against just 66% of those aged 45-54.

A place to call your own – Young Brits’ vision of success

The majority of millennials define success as simply having something you can call your own – 66% typically class success in the property market as owning your own home and funding it independently (41%); not having a large (20%) or expensive (13%) property.

However, owning your own home doesn’t come without being financially stable – 86% of those between 18-34 say admit this is important to them with the vision of achieving this between the ages of 25-34.

Interestingly, for 18-24 year olds; owning the perfect family home sits high on the list of life goals too. This age group are the most likely (than any other age group) to define success within the property market as ‘a great family home’ (51%), which they have funded independently (46%) – in comparison to less than a third (32%) of 35-44 year olds who believe this.

Home ownership

When taking a wider look at the whole of the UK, first direct found that the majority of Brits (64%) believe simply having a place to can call your own, no matter where it is or what it looks like, is the vision of success when it comes to property. Similarly, over a third (36%) also believe that success comes from funding your home independently.

‘Family is the heart of the home’ – second on the success scale is to have a great family home (37% said this is the measure of a successful home) and a similar amount of Brits (36%) measure a successful home by the desirability of the area. Brits admit having a large (12%) or expensive property (8%) is of little value when it comes to a home with both revealed as some of the least important measures of a successful home.

Joint Equity Shared Home Ownership can help many people make the break from renting or living with parents who would be excluded from home ownership because they have insufficient deposit or their income is too low for the new mortgage affordability tests.

More here