As Buy-to-Let loses tax relief, property investment alternatives become more desirable

I have long been a critic of buy-to-let, specifically about the unlevel playing field between landlords and homeowners.

Buy-to-let has always been popular but that is now changing

The chief concern has traditionally been the favourable tax treatment for buy-to-let. This has allowed landlords to offset many costs against rental income to lower their tax bills – the big one being mortgage interest which was removed from homeowners years ago.

Now I understand that when buy-to-let was conceived it was considered as a business and the principle behind that has always been that tax should only be charged on profits. So in the business of buy-to-let, mortgage interest and other allowable expenses are costs and therefore deducted before the profit is calculated.

That situation is changing as result of many landlords buying property not as a business but just as another property to maximise their capital gains.

“Ha ha” I hear you shout, that is a business – an investment business; but Chancellor George Osborne does not see it that way and has decided full-on mortgage interest income tax relief on buy-to-let was unfair or possibly a prime target for getting some extra tax in – and took the axe to it in his summer Budget.

He has also changed some allowable expenses such as the blanket 10% allowance for furnished properties which is also going.

Buy-to-let less attractive due to tax changes

But the big one is restricting buy-to-let mortgage tax relief to a maximum of 20%. This will diminish the attraction of buy-to-let. Yet Britain’s small army of cash-rich minor property investors still appear to be piling in. Especially as you can now take your pension out and do with it what you will.

This is a classic example of intervention by Government, for the right reasons, having often unforeseen consequences which requires another intervention:

- Release the shackles on pensions and we go and buy more property to rent out.

- By more potential landlords competing for property, owner occupiers are further priced out of the market.

- This means the would be home owner is driven into the very houses they are priced out of and the new landlords have just bought.

- This increases the UK rental trap that over 1 million people are currently in.

Buy-to-let mortgages easier to get

One of the temptations to become a landlord is the current very cheap buy-to-let mortgages. A new deal arrived this week, a two-year fix at just 1.84% from Accord. And this highlighted another place where the playing field is not quite level.

Most buy-to-let mortgages are interest-only, whereas most owner-occupiers must take out a repayment mortgage.

- On an interest-only basis, a £150,000 mortgage at 1.84% would have monthly payments of £230.

- On a repayment basis, monthly payments would be £628

Furthermore, across the mortgage industry, with MMR and affordability the same borrower is likely to find a buy-to-let application far less onerous than a residential one.

Budding landlords should be warned though – change is in the air.

They may find the rules are much tighter when it comes to remortgaging at the end of that two-year fix with the up coming EU changes to buy-to-let mortgage approval rules. But more of that in a future blog.

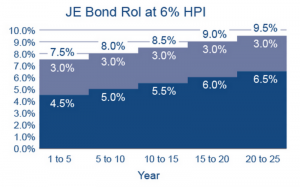

Of course the easy route into UK property for both home occupiers and investors has now become through Joint Equity and its associated Investment Bonds.

See www.jointequity.co.uk if you want to own your own home,

and www.jeips.uk if you want all the information about joining the ethical UK property investment revolution.

Brad Bamfield